The real thing about Islamic finance is that it is not only about Islamic finance. Islamic finance is in reality a peaceful contribution to a wider set of efforts aimed at the renaissance of Islam as a modern religion that has to co-exist in the modern world, with a multitude of interdependence of communities and mutuality of faiths.

Since 2010, GIFR has reported briefs on the state of affairs of the global Islamic financial services industry as an opening chapter of the annual report. During the last 11 years, the industry has gone through significant changes, particularly with reference to its growth. Following the tradition, this chapter provides an overview of major developments in Islamic banking and finance during the ongoing COVID-related pandemic.

COVID-19 has proven to be an extraordinary correction – dubbed as Great Reset by some observers – not only in the global markets but also as a phenomenon that has shaken the very basic fabric of the society – individual. Keeping aside the cynicism contained in the Great Reset thinking, everyone and everything in between has been affected by this disruption. While income disparities have apparently increased (with 120 million people pushed into extreme poverty and rather paradoxically increase in wealth of billionaires), gender diversity is at stake, child poverty has gone up, the future generations are going to feel the scars of the wounds it has inflicted on education. Loss of human lives will keep on reminding many who have been directly hit by this calamity. It may well be needed to reset a new date for achieving Sustainable Development Goals (SDGs). If not, the world would require lot more resources to be utilized more efficiently and timely manner to be even close to achieving the targets by 2030, let alone achieving the SDGs in entirety or individually.

Yet, it has so far caused only the second-largest global recession in the history, after the Great Depression of the 1930s!

The term disruption had variedly been used to refer to technological advancement, financial innovation and the price changes but COVID-19 has for sure given the true meanings to it. It is certainly the biggest disruption Islamic banking and finance (IsBF) has witnessed since the 1970s when it emerged as a formal phenomenon in some national financial markets. The oil shock of the early 1970s has by many been attributed as the real impetus to the birth of IsBF. It has since then experienced neo-colonization of the Arab world, with the occupation of Iraq and Afghanistan and increased influence of the Western powers in many Arab countries (see below for specific example of what has recently happened in Sudan). The so-called Arab Spring proved to be an impetus to birth and subsequent growth of IsBF in the countries affected by this phenomenon. The North African regimes had historically been hostile to IsBF. It is only after the Arab Spring that IsBF has started thriving in Libya, Algeria, Morocco and Tunisia. Furthermore, IsBF witnessed significant progress in countries like Syria and Iraq, which were not friendly towards it before the ongoing conflicts. Also, constitutionally secular states like Turkey and Indonesia are now explicitly vowing to be global centers of excellence for IsBF.

It has also survived the Global Financial Crisis (GFC) of the 2008-09. It not only survived during the GFC but its credentials as a sustainable financial system were further accentuated in its aftermath.

The disruption is the most comprehensive this time, with the two holiest mosques of Muslims nearly completely shut making it hard for the pilgrims to perform the rituals they have undertaken for centuries. Micro and small and medium enterprises (SMEs) have been very badly hit by the lockdowns. It is fair to assert that apart from public sector employees, almost everyone is hit hard by the pandemic. In some cases, national responses and plans to combat the adversary seem completely disoriented, and it seems as if the statement, “Everyone has a plan until they get hit,” by the famous boxer Mike Tyson aptly describes the situation. Malaysia – an important Islamic financial market – is a good example in this respect. The populace therein is completely bewildered by the inconsistencies in the government response to COVID-19. While the initial response of the Malaysian government was hailed as one of the best, its later treatment can at best be described as directionless, if not complete chaos. Obviously, it had implications for growth and development of IsBF therein.

“Everyone has a plan until they get hit”- Mike Tyson

Sudan – one of the two countries with a full-fledged Islamic economic system – announced re-introduction of the dual banking system, hence abandoning its long-standing policy of allowing only Islamic banks and financial institutions to operate in the country. The decision by the Sovereign Transitional Council is radical, as it may pave the way for re-emergence of an interest-based economic system. If that happens, this will be a major setback for the global movement of Islamisation of economies of the member countries of the Organization of Islamic Cooperation (OIC).

Interestingly, no official response has so far come from industry-building infrastructure bodies like Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), Islamic Financial Services Board (IFSB), International Islamic Financial Market (IIFM) and General Council for Islamic Banks and Financial Institutions (CIBAFI). IsDB has also opted to keep quiet on the matter. This confirms the fact that IsBF lacks a formal global advocacy platform and that it does not enjoy political support on a global level.

The lack of response to this anti-development may have far-reaching implications for further acceptance and adoption of IsBF by multilateral institutions like the World Bank, International Monetary Fund (IMF) and regional development banks. The initial enthusiasm of the multilateral institutions towards IsBF has already started receding, and the announcement by the Sudanese authorities as regards introduction of a dual banking system will certainly not help in this respect.

One should look at the future engagements of the multilateral institutions in Sudan to see if the new regime uses Islamic financial structures or opts for conventional arrangements while negotiating financial packages with them.

The need for a global body with an exclusive focus on advocacy is now paramount. Admittedly, CIBAFI was founded in 2001 for: (1) Advocacy of Islamic finance values and related policies and regulations; (2) Research and innovation; and (3) Training and professional empowerment. Over the years, the focus has moved to the last two stated objectives, with only a marginal focus on advocacy. As a body set up by IsDB and affiliated with the OIC, it possessed huge promise that has yet to be realized. There are hundreds of training providers, and the likes of Islamic Development Bank Institute are spearheading R&D in IsBF, a body like CIBAFI should exclusively focus on the advocacy of IsBF to play a more meaningful role as an industry infrastructure body.

“The need for a global body with an exclusive focus on advocacy is now paramount”

The problem with all the industry infrastructure bodies – not just CIBAFI – is that everyone is trying to do everything without any coherent and consistent approach. By way of example, AAOIFI has a growing training emphasis, something that could have been offered by another body like INCEIF and even Bahrain Institute of Banking and Finance (BIBF). It should not have been the function of AAOIFI to get involved in training at all beyond a limited training of trainers programme. AAOIFI should have an exclusive focus on standards development – accounting & auditing and Shari’a standards – and have a proactive role in pushing external providers to offer specific training programmes to promote their standards. Similarly, Islamic Financial Services Board (IFSB) must continue to focus on standards development in the area of regulation and supervision. So far, IFSB has proven to be most focused, and it may be due to the fact that it is headquartered in Kuala Lumpur that enjoys a more professional ecosystem for IsBF than many other cities/countries. IIFM has also in the last 10 years or so focused on the standardization of Islamic financial contracts. However, even in this case, publishing an annual Sukuk Report seems like stretching its scope too much.

Hence, it is recommended that a global advocacy forum should be developed comprising the representatives of various stakeholders, namely, IsDB, infrastructure bodies (AAOIFI, IFSB, CIBAFI and IIFM, etc.), national bodies like KNEKS in Indonesia, and market players (Islamic banks and other Islamic financial institutions). It is also important to engage other think tanks like Cambridge International Financial Advisory (Cambridge IFA), media specialists like Thomson Reuters, Redmoney and others that have been championing the cause of IsBF. It is also important to engage the academic community (which has by and large been sceptical of the IsBF practices). In this respect, the role of Cambridge IFA is commendable. It has been publishing this report – GIFR – since 2010 on an annual basis, which has advocated IsBF effectively. Furthermore, its Global Islamic Finance Awards (GIFA) has successfully engaged top political leaders – Prime Ministers and Presidents – by way of presenting to them Global Islamic Finance Leadership Awards. Similarly, there are a number of other smaller players in this domain, which should be brought on board to create an effective global advocacy platform.

How has the Industry Responded to the Pandemic?

There are certainly some positive developments associated with the outbreak of the pandemic and its persistence. The use of technology is a big win. It has allowed remote working not only possible, but it has now become a preferred choice for many employers and employees. The long-term effects of this on productivity have yet to be assessed and quantified.

COVID-19, however, has not dinted the industry uniquely or unevenly, as IsBF has reacted to the pandemic as well (or as bad) as its counterparts in the global and national financial markets5. The contribution of FinTech to the industry growth admittedly remains marginal. The industry pundits are, however, buoyant about the Islamic FinTech. There are quite a few reports focusing on the Islamic FinTech6. These are good examples of presenting the Islamic Fintech landscape in specific countries and worldwide.

Careful readings of these documents reveals that there is no Islamic FinTech initiative that may pose a serious threat to the traditional Islamic banks and financial institutions. Huge enthusiasm towards an Islamic cryptocurrency has now receded, bringing down the expectations of those who would like to jump up at the sight of any new thing on the horizon. Similarly, attempts to create Islamic Amazons have also licked the dust. Consequently, we now have more realistic expectations towards the role of FinTech in IsBF.

“The contribution of FinTech to the industry growth remains marginal.”

Amidst the mediocrity of thought and limitations on size and location, there are some promising FinTech initiatives that may revolutionize Islamic FinTech. Given that Islamic FinTech market has yet to come out of infancy, it is difficult to draw an authentic list of top performers in this field. ETHIS is perhaps the best example of an Islamic FinTech initiative that has grown organically since its inception. With 30,000+ members from over 50 countries, ETHIS has not only grown slowly but has also played an effective advocacy role.

FAIR is another emerging brand in Islamic FinTech. Based in the USA, it has impressive plans to implement an innovative strategy to create value. If successful, FAIR will offer a good example to emulate in other parts of the world. Central to the plan is a SPAC (Special Purpose Acquisition Company) that will serve as an engine for value creation. As COVID-19 is unique in many respects, it caught IsBF unprepared to respond to it. Consequently, the industry followed what the financial sector regulators prescribed for all the financial players in given markets and what governments rolled in out in terms of support programmes. Subsequent to enthusiasm in the likes of UAE, Bahrain and Malaysia in the pre-COVID era, KSA has emerged as a new focal player in Islamic FinTech amidst the pandemic. These markets, however, are limited by their size. The countries with dense populations (e.g., Indonesia, Pakistan, Bangladesh, Nigeria and to some extent Egypt) have huge potential for growth of Islamic FinTech. Indonesia is perhaps the most promising market in this respect, while other aforementioned countries have yet to witness any significant developments in Islamic FinTech.

Response to the COVID-19 in Pakistan – An Interesting Example

COVID-19 has not dinted the industry uniquely or unevenly, as IsBF has reacted to the pandemic as well (or as bad) as its counterparts in the global and national financial markets.

Let us look at Pakistan – one of the top 10 Islamic financial markets according to our Islamic Finance Country Index (IFCI) as reported in Chapter 2. The country recorded 30% growth in Islamic banking assets in 2020, along with growth of 27.8% in deposits. This was the highest annual increase in assets since 2012 and in deposits since 2015, withering away the impact of the pandemic. Financing by Islamic banking institutions – both fully-fledged Islamic banks and Islamic banking windows of conventional banks – also grew by 16%.

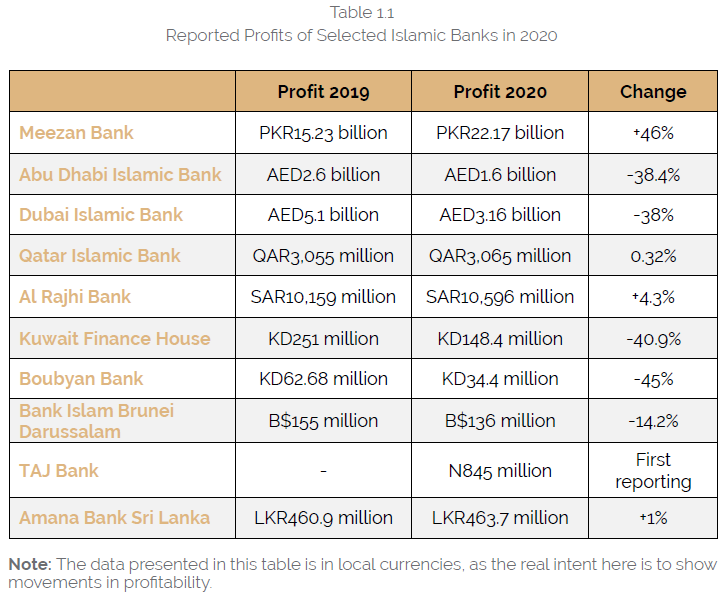

Meezan Bank – the largest Islamic bank in the country – registered 46% growth in profit after tax, with the end of the year 2020 profit of PKR22.17 billion as compared to the 2019 end-of-the-year figure of PKR15.23 billion. This is obviously a stellar performance in the wake of the pandemic. However, other Islamic banks around the world have not been that lucky as they reported significant drop in their profitability.

Table 1.1 reports profitability of randomly selected 10 Islamic banks.

Note: The data presented in this table is in local currencies, as the real intent here is to show movements in profitability.

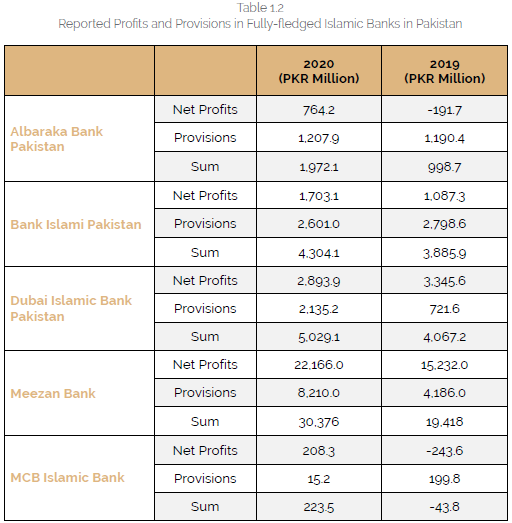

Meezan Bank tops the list in terms of profitability. While there is some visible drop in reported profitability of Islamic banks, it is primarily because of increased provisions in the wake of uncertainties owing to the length of the pandemic and its aftermath. This is certainly the case for Abu Dhabi Islamic Bank (ADIB), Dubai Islamic Bank (DIB) and Boubyan Bank as the banks’ other performance indicators showed improvement in the reported period. Most of these banks reported increase in assets, deposits and financing, reflecting on the health of fundamentals of their operations. As the focus in this section is on Pakistan, Table 1.2 provides a snapshot of profitability and provisioning in the five fully-fledged Islamic banks in the country.

Table 1.2 Reported Profits and Provisions in Fully-fledged Islamic Banks in Pakistan

Table 1.2 presents a very healthy state of affairs of Islamic banking in Pakistan, as all the fully-fledged Islamic banks have improved their profitability during the pandemic so far. Given the prudent provisioning, it is expected that Islamic banks will the pandemic whither away without leaving any bad assets on their balance sheets.

Future of IsBF in the Post-COVID Era

This report focuses on the future of Islamic finance in the post-COVID era. While it will take a long time to assess the real impact of COVID-19 on the global economy and its constituents, a lot of literature has already started starting emerging on the assessment of consequences of the pandemic on IsBF. Although most of the studies are rudimentary in nature, there are some documents that are worth reading to have a preliminary understanding of the issue. IsDB published a comprehensive report on the response of IsDB to the COVID-19 crisis. However, it is more like a theoretical framework than a script on policy response. Yet, it is a good reading.

What is the future of IsBF?

The cynic would not find any worthwhile value in IsBF. For them, it should have already gone into oblivion. But it hasn’t!

The captive user of Islamic financial services would present scores of reasons to argue in favor of the sustainability of IsBF. The most convincing argument, however, is based on statistical evidence. The industry has gone from strength to strength since its inception (see the next section). This must reflect on the bright future of IsBF. This report attempts to explore the future of IsBF in wake of growing interest in Islamic social finance. It is safe to assume that the pandemic will make IsBF more sensitive to the global social agenda. The present decade will see more emphasis on SDGs before the deadline of 2030, and Islamic banks and financial institutions are expected to show their commitment to these goals to garner wider appeal beyond their captive markets.

Size and Growth of the Global Islamic Financial Services

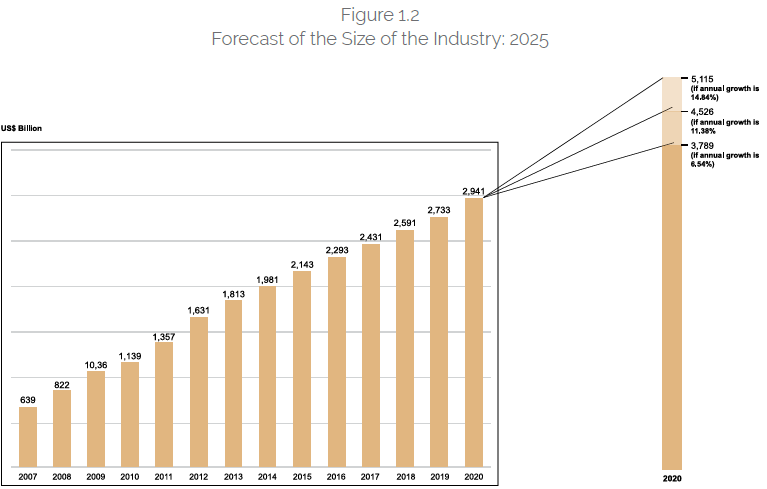

The global Islamic financial services industry nearly touched the historical milestone of US$3 trillion at the end of 2020. The estimated Islamic financial AUM as of December 31, 2020, was US$2.941 trillion, exhibiting annual growth of 7.61% (see Table 1.3), which is also the highest annual increase in the last 5 years. This is interesting, as the industry managed to pull up the growth rate from the previous year’s growth of 5.48%, despite the international restrictions on mobility and national lockdowns of economies. This may tentatively suggest that the pandemic has not (at least as yet) affected the industry unfavourably.

The GFC killed Islamic financial innovation, hence limiting the growth of the industry

This is in contrast to the previous such shocks like the GFC of 2008-09, which certainly dragged the growth of the industry, compelling the industry observers to revise their forecasts for the industry size of US$6.5 trillion to less than half of it. The GFC actually killed any significant trends in Islamic financial innovation, hence limiting the growth of the industry. Arguably, the industry must have doubled its current size had it not been hit by the GFC.

The current pandemic, on the other hand, has widened the scope of innovation by way of pushing the Islamic finance think tank to start looking into new avenues of growth, especially in areas like Islamic social finance. It is expected that the sukuk related with CSG, Green, SDG and COVID-19 Response will play an important role in the next five years.

Table 1.3 The Global Islamic Financial Services Industry: Size & Growth

| AUM (US$ Billion) | Growth (Annual %) | Average accumulative growth (%) | |

| 2007 | 639 | ||

| 2008 | 822 | 28.64 | 28.64 |

| 2009 | 1,036 | 26.03 | 27.34 |

| 2010 | 1,139 | 9.94 | 21.54 |

| 2011 | 1,357 | 19.14 | 20.94 |

| 2012 | 1,631 | 20.19 | 20.79 |

| 2013 | 1,813 | 11.16 | 19.18 |

| 2014 | 1,981 | 9.27 | 17.77 |

| 2015 | 2,143 | 8.18 | 16.57 |

| 2016 | 2,293 | 7.00 | 15.51 |

| 2017 | 2,431 | 6.02 | 14.56 |

| 2018 | 2,591 | 6.58 | 13.83 |

| 2019 | 2,733 | 5.48 | 13.14 |

| 2020 | 2,941 | 7.61 | 12.71 |

| Average growth (2009-20) | 11.38 | ||

| Average growth (2009-15) | 14.84 | ||

| Average growth (2016-20) | 6.54 | ||

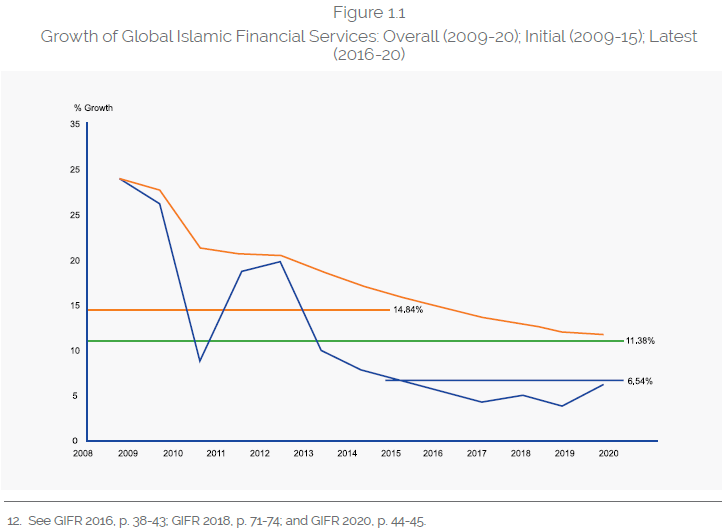

Figure 1.1 depicts an interesting story. Since 2019, the global Islamic financial services industry has on average grown by 11.38% per annum, which itself seems impressive. However, the major contribution to it has come from the earlier years (2009-15 when the average growth was 14.84% per annum). However, the industry has significantly slowed down in the last five years, achieving only 6.54% annually. Is it something to worry about?

“The current pandemic has widened the scope of innovation, especially in areas like Islamic social finance”

The previous editions of GIFR have reported various reasons for the slowdown in the growth.

The main reasons reported previously were:

In addition, in GIFR 2020, we alluded to the possible adverse effect of COVID-19 on IsBF, suggesting that it could put a drag on the growth of the industry in the years to come. However, 2020 statistics do not confirm any negative effect on the growth, as Islamic banks and financial institutions continue to grow despite very difficult market conditions. The good news is that there are greater prospects of growth, presented by an increased focus on FinTech and through it on financial inclusion. Despite having become visible segments of financial services sectors in a number of countries, IsBF has yet to become a dominant force in most of the countries where it exists with a degree of significance. Looking at the Islamic financial sectors of the countries comprising the Gulf Cooperation Council (GCC), we find that IsBF in these countries has yet to surpass 50% market share in the region excluding Saudi Arabia.

There are three purely statistical forecasts of the size of the global Islamic AUM in 2025. If the industry recaptures pre-2015 annual growth rates (highly unlikely, given the current market conditions), the global Islamic AUM is expected to stand at US$5.115 trillion by the end of 2025. The size will be US$4.526 trillion if the industry grows annually with average growth rate of 11.38% (2010-20). This is a likely outcome. However, if the growth remains consistent with the last five years’ annual growth rate, the industry size is expected to be US$3.789 trillion (highly likely). Another realistic forecast could be based on the weighted average of the annual growth rates in 2010-15, 2010-20 and 2016-20, with respective weights of 0.2, 0.3 and 0.5. This gives a forecasted figure of US$4.275 trillion.

So, in the worst scenario, the industry will still continue to grow, albeit at a slower rate. From this viewpoint, there is little to worry about. However, as we have pointed out in previous editions of GIFR, the gap between actual Islamic AUM and potential Islamic AUM13 will continue to grow. The volume of the size gap must indicate of failure of the industry to meet all of the potential demand for IsBF.

Global Islamic financial services industry is segmented into:

Which segment has contributed most to the growth of global Islamic AUM?

Interestingly, the industry grew more in 2020 (during the pandemic) than immediately before the advent of COVID-19. The Islamic capital markets contributed the most to growth of Islamic financial assets during 2020, particularly sukuk issuance remained resilient to the pandemic.

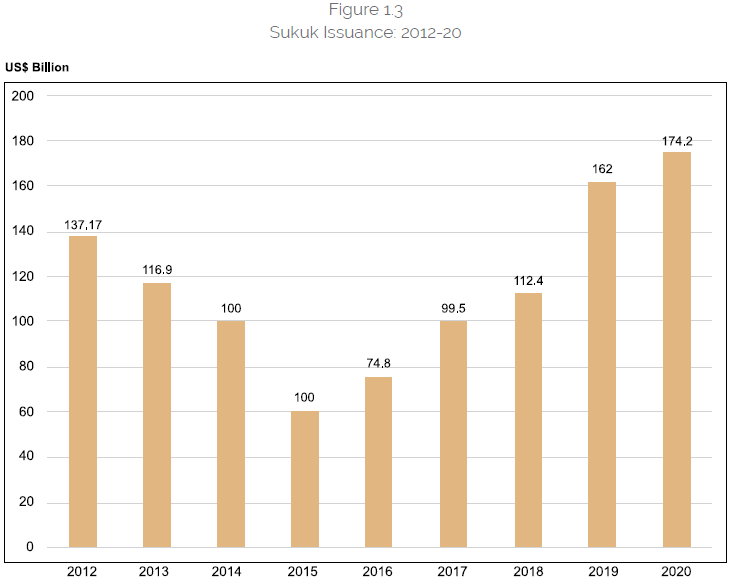

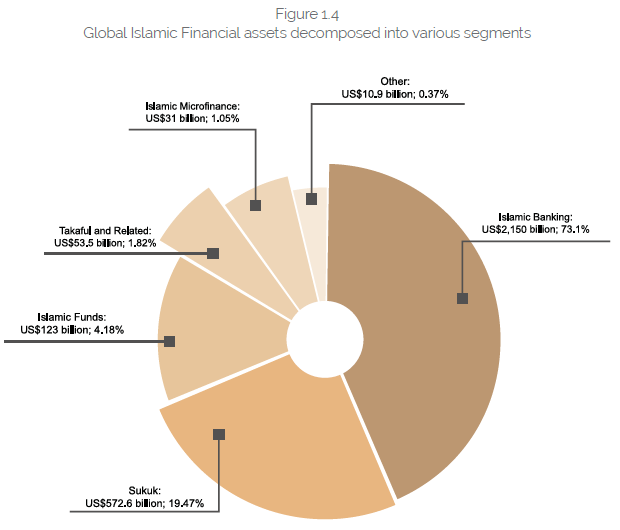

Improvement in reporting of IsBF in a number of countries (e.g., Indonesia and Pakistan) has contributed to visible increase in share of Islamic capital markets in the global Islamic AUM. Nevertheless, the value of sukuk outstanding at the end of 2020 was noted to be US$572.6 billion, up from US$476 billion reported for 2019 in GIFR 2020 (an annual growth of 16.9%). This has also resulted in the share of sukuk in the global Islamic AUM from 17% at the end of 2019 to 19.47% at the end of 2020.

The sukuk issuance experienced another bumper year, following the record volume of issuance in 2019 (US$162 billion), making a new record of annual issuance of US$174.2 billion in 2020.

This was followed by Islamic banking assets, which totaled US$150 billion at the end of 2020 and contributed slightly over 73% to the global Islamic AUM. Figure 1.4 also shows that the shares of Islamic asset management, takaful and Islamic microfinance remain low or negligible.

While sukuk continue to capture greater share in the global Islamic AUM, and hence growing importance in the industry, some concrete measures must be taken to grow other sectors. As mentioned above, Islamic social finance is a perfect fit in the present pandemic-hit environment. GIFR 2020 focused on this aspect, and this year’s theme of the report – Islamic Finance in the Post-COVID Era – attempts to re-emphasize this point.

Moving the industry from the worst scenario in 2025 (US$3.785 trillion) to the best (US$5.115 trillion) would require a re-orientation of the industry in favor of Islamic social finance. Otherwise, Islamic banking will continue to feature prominently in IsBF.

IsBF, Crises and Growth

Is there something inherent in IsBF that makes it excel when facing a serious challenge?

Contrary to some popular views held by the enthusiastic advocates of IsBF14, there is little inherent to it that makes it stronger, more stable and superior to its conventional counterpart. At least in practice if not in theory!

The recent growth in Islamic financial assets may be explained with reference to the developments in Islamic capital markets: an accentuated focus on mergers and acquisitions (M&A) and the issuance of sukuk (already discussed above). Also, improvements in Islamic financial intelligence have brought more information on the Islamic financial practices that were not previously captured by the reported data (see below an example of Indonesia).

M&A and Consolidation in IsBF

Perhaps the most phenomenal M&A activity in IsBF during the reported period has been witnessed in Indonesia where three Islamic banks were merged in an attempt to eventually create a potential ‘mega Islamic bank’ in the Far Eastern region. Before that, Dubai Islamic Bank (DIB) completed full acquisition of Noor Bank to empower DIB as an influential Islamic financial player in the GCC region. There are some other high-profiled M&A deals are in the pipeline, which have inevitably been delayed due to the ongoing crisis. The merger of three state-owned Islamic banks– BNI Syariah, Bank Syariah Mandiri and BRI Syariah – to form Bank Syariah Indonesia (BSI), Indonesia’s largest Islamic bank, was a hallmark of 2020. This gave prominence to Islamic banking in the country, as BSI emerged as one of the top 10 banks in Indonesia and one of the top 10 Islamic banks in the world (in terms of market capitalization).

However, M&As are not a source of growth in Islamic banking or overall Islamic financial assets. With the moves like BNI-BSM-BRI merger, Indonesia merely consolidated Islamic financial assets. In case of Indonesia, the boost to growth has come from other sectors, particularly capital markets. Also, a systematic approach to hajj-related savings has also boosted Indonesia’s ambition to capture higher Islamic finance market share.

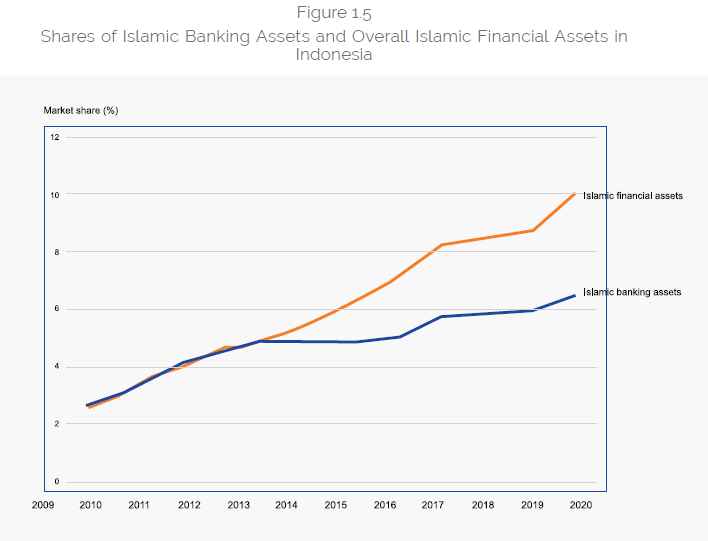

Figure 1.5 depicts this phenomenon. Since 2009, there has been a graduate increase in Islamic banking assets in Indonesia but since 2017 (when statistics on overall Islamic financial assets in the country started becoming more readily available), there has been significant growth in overall Islamic financial assets. This phenomenon may be referred as ‘publicity of Islamic financial intelligence.’ Saudi Arabia is another example of a country where publicity of Islamic financial intelligence has started emerging, following a concerted focus on Islamic banking by the Saudi Central Bank. There is a need to highlight the importance of publicity of Islamic financial intelligence in other markets like Pakistan that has so far focused on reporting Islamic banking assets and related statistics only, maintaining a relative neglect of reporting on Islamic capital market therein.

Conclusion

The IsBF market remains healthy. The growth of Islamic AUM has started picking up, despite tough conditions in the markets. To maintain the momentum, a shift away from the Islamic banking sector (in favor of other industry segments) is required. Islamic social finance may prove to be a viable contender to spur further growth in IsBF.

Although our previous suggestions in GIFRs 2010-2020 to devise a global strategy for the growth of IsBF have not received any favourable response from various stakeholders, it must be reiterated that in the absence of such a strategy – or global roadmap – boosting growth in IsBF will remain a challenge. National roadmaps and strategies have worked in some cases but they have not been able to bring a significant change on the global horizon.

The closure of Dubai Centre of Islamic Banking and Finance is one example of failure of a national approach to benefitting from the global Islamic financial services industry. There is no better institution than IsDB to spearhead such a global strategic framework for the growth of IsBF, with a special focus on its 57 member countries.

{kind=link}